Transition to new mandatory ACCC merger notification regime commences

Market Insights

Key Points

- The 6 month transition period to the new mandatory ACCC merger notification regime (Mandatory Notification Regime) commenced on 1 July 2025. During this period, if parties enter into a transaction that will meet the notification thresholds and complete on or after 1 January 2026:

- there will be important strategic decisions for merger parties as to whether to seek ACCC clearance under the current informal merger regime or voluntarily notify under the new regime; and

- informal merger clearance applications made after October 2025 risk not being considered by the ACCC before the informal review system shuts down at the end of the year. If this happens, the acquisition may need to be re-notified under the Mandatory Notification Regime.

- Treasury has finalised the Competition and Consumer (Notification of Acquisitions) Determination 2025 (Determination), which sets out the thresholds and some exemptions for determining which acquisitions require notification under the Mandatory Notification Regime, as well as the notification forms and filing fees.

- The ACCC has also issued updated guidelines in relation to the Mandatory Notification Regime; however, some important gaps remain including in relation to the proposed merger notification waiver process.

Recap – what is the Mandatory Notification Regime?

Australia is transitioning from its current informal and voluntary merger clearance regime to a new Mandatory Notification Regime – see our previous articles here and here.

Any acquisition of shares or assets that meets relevant notification thresholds and will be put into effect after 1 January 2026 must be notified to the ACCC and cannot be completed unless and until the ACCC determines that the transaction may be put into effect. Failure to comply with these requirements will mean the transaction is void and may also result in penalties of up to $50 million, three times the benefit of the illegal conduct or 30% of Australian group turnover.

Transition period has now commenced

The Mandatory Notification Regime will apply to acquisitions put into effect after 1 January 2026, even if the agreement for the acquisition was signed well before that time. A transition period commenced on 1 July 2025 and will continue until 31 December 2025 (Transition Period), during which:

- businesses can either voluntarily ‘opt in’ to the Mandatory Notification Regime or seek informal merger clearance under the current regime; and

- if a business obtains informal merger clearance, the transaction will not be required to be notified under the Mandatory Notification Regime, provided that it is put into effect within 12 months of the date of ACCC informal clearance.

However, the ACCC has warned that informal merger clearance applications which are lodged between October and December 2025 risk not being considered by the ACCC before the commencement of the Mandatory Notification Regime. This means that the acquisition may need to be re-notified under the Mandatory Notification Regime if it meets the notification thresholds and will be put into effect on or after 1 January 2026.

Accordingly, there will be important strategic decisions for merger parties in the lead up to 1 January 2026 as to which ACCC clearance route may be most appropriate for a particular transaction, as well as corresponding implications for transaction timelines and documentation (eg ACCC condition precedents).

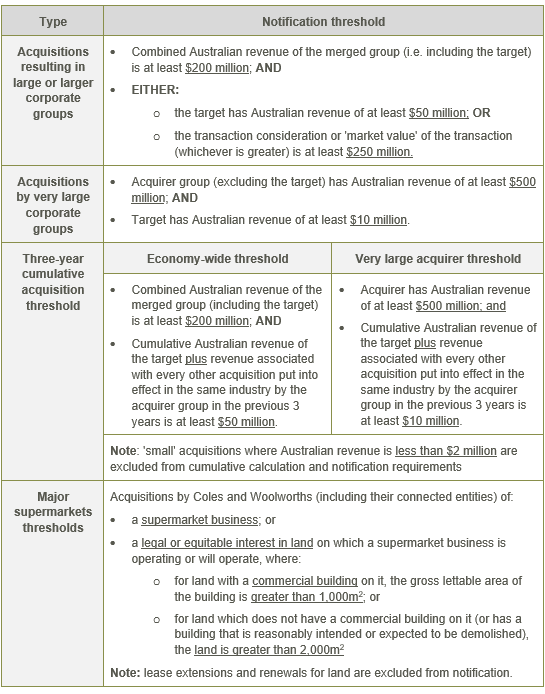

Notification thresholds clarified

The Determination sets out the following thresholds, with the monetary amounts consistent with the previous draft thresholds released by Treasury but with some important changes to the measure of revenue used for the calculation:

The Determination clarifies that, in calculating a party’s revenue for the purposes of the notification thresholds:

- ‘Australian revenue’ is an entity’s gross revenue for its most recently ended 12 month financial period, determined in accordance with accounting standards, that is attributable to transactions or assets within Australia, or transactions into Australia. The concept of ‘GST turnover’ that was included in the previous draft Determination has been removed;

- Australian revenues are calculated as at the contract date for:

- the acquirer and acquirer’s connected entities; and

- the target and target’s connected entities being directly or indirectly acquired;

- ‘connected entity’ includes related entities (within the meaning of s4A of Competition and Consumer Act) and controlled entities (adopting definitions of ‘control’ in s50AA and ‘associates’ in Chapter 6 of Corporations Act); and

- in the case of an asset acquisition (as opposed to a share purchase), the revenue to consider is the Australian revenue of the target to the extent that it is attributable to the asset. If it is not reasonably practicable to attribute the Australian revenue of a target to an acquisition of an asset, the amount to be included is instead 20% of the market value of an asset.

Exemptions to the notification requirements clarified

There are various exemptions to the mandatory notification requirements, including:

- acquisitions that do not result in control (ie capacity to determine the outcome of decisions about another entity’s financial and operating policies);

- internal restructures and re-organisations;

- acquisitions of listed companies, listed schemes and large unlisted companies (ie ‘Chapter 6’ acquisitions) which do not result in the acquirer holding more than 20% of voting rights; and

- acquisitions made in the ordinary course of business, except where the asset is land or a patent.

The Determination contains a number of further clarifications and additions to exemptions to the notification requirements, including the following:

- Certain land acquisitions –

- acquisitions of a legal or equitable interest in land:

- where the purpose is to develop residential premises; or

- by a business primarily engaged in buying, selling, leasing or developing land for a purpose other than to operate a commercial business on the land (unless it is ancillary or incidental to the primary purpose of buying, selling, leasing or developing the land);

- acquisitions of an interest (including a share) in a ‘land entity’, where the entity’s only non-cash asset is a legal or equitable interest in land and the holding of that land is for one of the purposes set out above;

- renewals and extensions of leases;

- acquisitions of a legal interest or further equitable interest in land after an initial equitable interest was previously notified (provided that the size of the land is materially the same and the proportion of ownership interest is the same);

- acquisitions that relate only to a sale and leaseback arrangement in relation to land; and

- acquisitions of land development rights.

- acquisitions of a legal or equitable interest in land:

- Liquidation, administration, receivership – acquisitions made in a person’s capacity as an administrator, receiver, receiver and manager or liquidator;

- Financial market infrastructure, debt, money lending and security interests – certain acquisitions:

- of shares or assets by an operator or participant of a clearing and settlement facility;

- in the context of capital raising activities, such as rights issues, buy-backs, and dividend reinvestment and underwriting of fundraising; and

- of:

- shares or assets as a result of an exercise of a right under the contract to close out any transaction relating to the contract, or exercise a right of set-off or combination of accounts under the contract;

- derivatives; or

- shares or assets that are (or are directly connected with) debt instruments or debt interests in an entity, part of an asset securitisation arrangement or financing transaction, or security interest, provided that the acquisition does not have the effect that a person will begin or can begin to control an entity that it did not previously control, or will or can acquire all (or substantially all) of the assets of a business;

- Nominees and other trustees – acquisitions of certain interests in securities by bare trustees or by a provider of a custodial or depository service; and

- Acquisitions by operation of law – acquisitions that take place by operation of a law of the Commonwealth, State or Territory (eg certain matters under succession laws).

Notification forms and information requirements

The Determination includes some adjustments to earlier drafts of the ‘short’ and ‘long’ form notification forms, which prescribe the documents and information which must be provided when lodging a notification. Overall, the information required to be provided upfront to the ACCC remains significant and exceeds the level of information typically provided upfront under the current regime.

The Determination also includes new sections setting out the information and documents required for a public benefit application and an application for a review of the ACCC’s decision by the Australian Competition Tribunal. However, the information and documents that will be required to be provided for a merger notification waiver application has not yet been released.

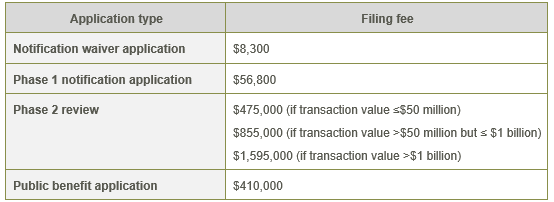

Filing fees

The Determination sets out the following filing fees for the Mandatory Notification Regime, which are significant and have the potential to impact the commerciality of some smaller to medium sized deals, particularly if a Phase 2 merger review is required:

ACCC has issued updated guidance

The ACCC has also released updated guidance to coincide with the commencement of the Transition Period, including ACCC interim merger process guidelines, ACCC final merger assessment guidelines and updated ACCC merger reform FAQs. However, as with the Determination, there remain some important gaps, including in relation to the proposed merger notification waiver process.

Next steps

As set out above, there will be important strategic decisions to be made by merger parties for the remainder of 2025 as to which approach to ACCC clearance route may be most appropriate for a particular transaction, as well as corresponding implications for transaction timelines and documentation (eg ACCC condition precedents).

There also remains some uncertainty regarding some key aspects of the Mandatory Notification Regime, including details regarding the proposed merger notification waiver process, which we will continue to monitor as more information becomes available.

How can we help?

We have a specialist competition and consumer law team that has considerable experience in all matters relating to competition and consumer law, including ACCC merger clearance advice and processes. If you would like more information about the services we provide, please contact us.

This article was written by David Fleming, Partner.

Subscribe for publications + events

HWLE regularly publishes articles and newsletters to keep our clients up to date on the latest legal developments and what this means for your business. To receive these updates via email, please complete the subscription form and indicate which areas of law you would like to receive information on.

* indicates required fields