New mandatory merger notification regime: Further details released

Market Insights

Key points

- More detail released: Multiple documents have been released providing more detail about the new mandatory and suspensory merger regime that will apply to acquisitions put into effect from 1 January 2026 (Mandatory Notification Regime). These include draft notification thresholds, notification forms, ACCC process guidelines and ACCC merger assessment guidelines.

- Notification thresholds confirmed: The draft notification thresholds are consistent with Treasury’s previous proposals. In addition, Coles and Woolworths will be required to notify almost all acquisitions of supermarkets and supermarket sites.

- Land and leases exemptions: Notification exemptions will apply for renewals and extensions of existing leases, and for acquisitions of land for development purposes.

- Notification forms: Draft ‘short’ and ‘long’ notification forms have been released. Both require provision of substantial information and documents, but the long form is more onerous. For ‘horizontal’ mergers, the ACCC proposes to require the ‘long’ notification form if the merger will create a market share of more than 20% if the increase is more than 5%, or a market share more than 40% if the increase is more than 2%.

- ACCC process guidelines: The ACCC has released draft merger process guidelines. These include an emphasis on pre-notification engagement with the ACCC and raise the potential availability of waivers for acquisitions that do not raise significant competition law issues (similar to ‘pre-assessment’ under the current regime).

- Draft merger assessment guidelines: The ACCC has released draft guidelines explaining its proposed approach to analysing acquisitions under the Mandatory Notification Regime. These place increased emphasis on creeping acquisitions, acquisitions which ‘create, strengthen or entrench’ a substantial degree of market power, and ‘killer’ acquisitions which remove a potential or nascent competitor and acquisitions involving multi-sided platforms.

- Transition arrangements: From 1 July to 31 December 2025 (Transition Period), business can voluntarily ‘opt in’ to the Mandatory Notification Regime or seek informal clearance under the current regime. If the ACCC grants an informal clearance under the current system during the Transition Period, the transaction will be exempt from the Mandatory Notification Regime provided it is put into effect within 12 months of the date of the informal clearance.

- Uncertainties remain: Perhaps the biggest takeaway from the recent raft of documents and guidelines is that significant uncertainties remain about the new regime. For example:

- there is still no information about what information, documents or forms the ACCC will require to assess a waiver application;

- it is not clear how the notifications thresholds should be applied to certain types of acquisitions. For example, it is not clear how the GST turnover of, say, a freehold or leasehold interest in a greenfield site which has yet to be developed (and may not be for some time) should be calculated; and

- ACCC clearance is required before acquisitions which meet notification thresholds can be ‘put into effect’. However, there is still uncertainty about what constitutes ‘putting an acquisition into effect’, particularly in circumstances where there may be several acts which constitute putting an acquisition into effect over a long period of time.

Recap: What is the Mandatory Notification Regime?

Australia is transitioning from its current informal and voluntary merger clearance regime to a mandatory and suspensory administrative merger regime (Mandatory Notification Regime). See our previous article on the Mandatory Notification Regime here.

Any acquisition of shares or assets that meets relevant notification thresholds and will be put into effect on or after 1 January 2026 must be notified to the ACCC and cannot be completed unless and until the ACCC determines that the transaction may be put into effect. Failure to comply with these requirements will mean the transaction will be void and may also result in penalties of up to $50 million, three times the benefit of the illegal conduct or 30% of Australian group turnover.

What’s the latest?

There have been a number of recent announcements, documents and guidelines released for consultation by Treasury and the ACCC which provide further details on how the Mandatory Notification Regime is proposed to work, including:

- exposure draft of the Competition and Consumer (Notification of Acquisitions) Determination 2025 (Draft Determination), which will set out which acquisitions require notification (eg notification thresholds, exceptions and waivers) and the notification forms that will need to be completed for a notification to be valid;1

- ACCC guidelines on the transition from the current merger regime to the Mandatory Notification Regime;2

- ACCC draft merger process guidelines;3

- provisional ACCC guidance for long form notification criteria;4 and

- ACCC draft merger assessment guidelines.5

We summarise key insights from these documents below.

Draft notification thresholds clarified

The Draft Determination sets out the following draft notification thresholds, which are largely consistent with Treasury’s previous proposals:

The Draft Determination also clarifies that, in determining a party’s turnover for the purposes of the notification thresholds:

- ‘GST turnover’ means the sum of the values of all the supplies that the entity made or is likely to make in the period of 12 months ending with the current month (excluding certain supplies, such as input taxed supplies, supplies that are not for consideration and supplies that are not made in connection with a business or other enterprise that the entity carries on);6

- in the case of an asset acquisition, the turnover of the asset is the GST turnover of the target attributable to that asset. In the context of leasehold acquisitions, Treasury has previously suggested that the turnover attributable to the lease would be the ‘lease income’;7 and

- GST turnover calculations must include, for the acquirer, each of the acquirer’s connected entities and, for the target, each of the target’s connected entities except those entities not being directly or indirectly acquired as a result of the acquisition. In broad terms, an entity (first entity) is a connected entity of another (second entity) if the second entity is an ‘associated entity’ of the first entity for the purposes of section 50AAA of the Corporations Act 2001, or the first entity controls the second entity.8

Exceptions to the notification requirements

The Draft Determination contains a number of exceptions to the notification requirements, including the following:

- Certain land acquisitions – acquisitions of a legal or equitable interest in land where:

- the purpose is to develop residential premises on the land, or the acquirer is a business primarily engaged in buying, selling or leasing land and the acquisition is for a purpose other than to operate a commercial business on the land; or

- the acquisition is an extension or renewal of a lease for land upon which a commercial lease is currently being operated;

- Liquidation, administration, receivership – acquisitions made in a person’s capacity as an administrator, receiver, receiver and manager or liquidator;

- Succession – acquisitions that take place solely because of a testamentary disposition, intestacy or a right of survivorship under a joint tenancy;

- Financial securities – acquisitions in the context of certain capital raising activities, such as rights issues, buy-backs and dividend reinvestment and underwriting of fundraising;

- Money lending and financial accommodation – acquisitions of certain of security interests;

- Nominees and other trustees – acquisitions of certain interests in securities by bare trustees; and

- Exchange rate derivatives – acquisitions of certain exchange rates derivatives.

Draft notification forms and information requirements

The Draft Determination includes draft ‘short’ and ‘long’ notification forms which prescribe the documents and information which must be provided to the ACCC when lodging a notification. The information required to be provided upfront to the ACCC is significant and likely to exceed the level of information typically provided under the current informal clearance regime.

Both forms require information regarding the merger parties, the proposed acquisition, acquisitions put into effect in the past three years, competitive effects (eg products or services supplied, market definition and shares), competitor and customer contacts, any goodwill protection provisions and various documents (eg transaction documents, financial documents and organisational charts). There is also a very broad category of ‘any other information or documents that would reasonably be considered by an objective third party to be relevant to the ACCC’s assessment of the acquisition’.

The ‘long’ notification form requires further information including in relation to the parties, details of the sale process and alternative proposals in the last 12 months, barriers to entry and other competitive dynamics, additional responses depending on whether the acquisition is horizontal, vertical or conglomerate, and more onerous documentary requirements. For example, board documents in the last three years not only in relation to the acquisition (eg describing the rationale or assessing or analysing the acquisition or valuation of the target) but also which ‘describe or analyse the competitive conditions or market conditions, market shares, competitors, or the business plans of a party in relation to the relevant products or services’.

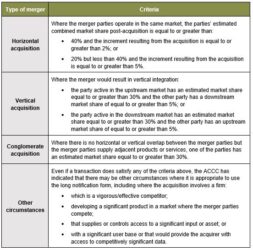

The ACCC has released provisional guidance that the long form notification should be used in the following broad range of circumstances:

ACCC transitional guidelines

The ACCC has released guidelines intended to assist businesses in managing the transition from the current voluntary and informal merger regime to the Mandatory Notification Regime. In summary:

- from 1 July 2025 to 31 December 2025 (Transition Period), businesses can voluntarily ‘opt in’ to the Mandatory Notification Regime or seek informal merger clearance under the current regime; however, businesses will not be able to lodge new merger authorisation applications during the Transition Period;

- informal merger clearance applications under the current regime which are lodged between October and December 2025 risk not being considered by the ACCC before the commencement of the Mandatory Notification Regime. If informal merger clearance is not obtained by 1 January 2026, the acquisition must be notified under the Mandatory Notification Regime (provided that it meets the notification thresholds and is not otherwise exempt or subject to a waiver);

- if a business obtains informal merger clearance from the ACCC within the Transition Period, the transaction is not required to be notified under the Mandatory Notification Regime provided that it is put into effect within 12 months of the date of ACCC informal clearance (12 month protection); and

- if a business receives informal clearance from the ACCC under the current regime before the Transition Period (ie before 1 July 2025), the 12 month protection does not apply. However, the ACCC has indicated businesses can ‘request an updated informal view’ for such transactions within the Transition Period which, if granted, will afford the merger parties with the 12 month protection.

Accordingly, there will be important strategic decisions to be made by merger parties in the lead up to 1 January 2026, as to which approach to ACCC clearance may be most appropriate for a particular transaction.

Draft ACCC merger process guidelines

The ACCC has released draft merger process guidelines for the Mandatory Notification Regime (Draft Process Guidelines).9 The Draft Process Guidelines largely summarise the legislation and explanatory memorandum for the Mandatory Notification Regime and some important details remain unclear. However key insights include the following:

- Pre-notification engagement with the ACCC: The ACCC encourages businesses to engage with it at least two weeks before formally lodging a notification, or ‘much earlier’ for more complex transactions or where remedies are proposed. In this context, it appears that ‘much earlier’ could mean months in advance. Given the ACCC review timeline will not commence until a valid notification has been received, this will add to transaction timing;

- Notification waiver process remains unclear: The Draft Process Guidelines provide little guidance on the notification waiver process, including the types of information that the ACCC will require to assess a waiver application (noting that Treasury’s Draft Determination also left a placeholder for waiver requirements). However, the guidance which is included suggests that the notification waiver process:

- is intended to be used for acquisitions which are unlikely to meet the notifications thresholds or do not raise competition risks which require further investigation. In this regard, the notification waiver process appears to be the Mandatory Notification Regime’s non-confidential equivalent of the ‘pre-assessment’ process under the current voluntary and informal merger regime; and

- could be more involved than many anticipated, which may limit its practical utility. For example, while the ACCC expects that most waiver applications will be determined within 20 business days, waiver applications will be placed on the Acquisitions Register (ie they will not be confidential) and the ACCC will not make a determination for at least 10 business days to allow third parties an opportunity to comment;

- ACCC’s broad powers to stop the clock: The ACCC can ‘stop the clock’ and extend determination timeframes for notified acquisitions (eg where the ACCC requests additional information and the merger parties fail to respond within the ACCC’s requested timeframe). However, there is little practical guidance on how the ACCC intends to exercise its discretion in these circumstances; and

- Very limited ability to seek confidential review: There are only two types of transactions that the ACCC can assess confidentially, being certain surprise hostile takeovers and voluntary transfers of authorised deposit-taking institutions and other regulated entities. All other notified transactions (and notification waiver applications) will be published on the Acquisitions Register and third parties will be given an opportunity to engage with the ACCC about the transaction. However, the ACCC will not publish third party submissions on the Acquisitions Register.

Draft merger assessment guidelines

The ACCC has released draft guidelines explaining its approach to analysing the potential effects of mergers and acquisitions on competition under the Mandatory Notification Regime (Draft Assessment Guidelines)10. The Draft Assessment Guidelines are similar in many respects to the ACCC’s current merger guidelines.11 However, there are new emphases on creeping/serial acquisitions, acquisitions that create, strengthen or entrench a substantial degree of market power, acquisitions which remove a potential or nascent competitor (also known as a ‘killer acquisition’) and acquisitions involving multi-sided platforms.

Next steps

As set out above, significant uncertainties remain regarding a number of aspects of the Mandatory Notification Regime, with various draft legislative instruments and ACCC guidelines still in consultation phase, and the government in caretaker mode with the upcoming election. We will continue to monitor developments as additional information becomes available.

Nonetheless, given the ACCC’s transitional guidelines, there will be important strategic decisions to be made by merger parties for the remainder of 2025 as to which approach to ACCC clearance may be most appropriate for a particular transaction, as well as corresponding implications for transaction timelines and documentation (eg ACCC condition precedents).

How can we help?

We have a specialist competition and consumer law team that has considerable experience in all matters relating to competition and consumer law, including ACCC merger clearance advice and processes. If you would like more information about the services we provide, please contact us.

This article was written by David Fleming, Partner and Alexander Shepherd, Senior Associate.

1 https://treasury.gov.au/consultation/c2025-644619

2 https://www.accc.gov.au/business/mergers-and-acquisitions/transition-to-a-new-merger-control-regime

3 https://www.accc.gov.au/media-release/new-merger-process-guidance-released-for-consultation

4 provisional-guidance-criteria-long-form-notifications.pdf

5 https://www.accc.gov.au/media-release/accc-consults-on-assessment-guidelines-for-new-merger-regime

6 See section 188-15 of the A New Tax System (Goods and Services Tax) Act 1999 (Cth).

7 Merger Notification Thresholds Consultation Paper dated 30 August 2024, p 13.

8 For the meaning of ‘control’, see s 50AA of the Corporations Act 2001, as modified by s 51ABS(2) of the Competition and Consumer Act 2010 (Cth) (as amended by the Treasury Laws Amendment (Mergers and Acquisitions Reform) Bill 2024 (Cth)).

9 https://www.accc.gov.au/system/files/merger-reform-merger-process-guidelines.pdf

10 https://www.accc.gov.au/system/files/merger-reform-merger-assessment-guidelines.pdf

11 https://www.accc.gov.au/system/files/Merger%20guidelines%20-%20Final.PDF

Subscribe for publications + events

HWLE regularly publishes articles and newsletters to keep our clients up to date on the latest legal developments and what this means for your business. To receive these updates via email, please complete the subscription form and indicate which areas of law you would like to receive information on.

* indicates required fields