A trust cloning renaissance

Market Insights

Clients living through succession planning and/or family breakdown may be surprised to learn that the options for tax relief are limited. It probably comes as more of a surprise when they realise tax could become payable to the ATO even when no cash is exchanged between the parties.

Enter the trust rollover under sub-division 126-G of the ITAA 1997 Income Tax Assessment Act 1997 (ITAA 1997).

Sub-division 126-G of the ITAA 1997 permits trust cloning in certain circumstances. It broadly requires the following elements to be satisfied, making clients to be eligible for relief:

(a) there is a transferring trust (Transferor) and a receiving trust (Recipient);

(b) the Recipient is a new trust, or an existing trust with only a small amount of cash or debt;

(c) both trusts have the same beneficiaries and the same membership interests. The trusts cannot be discretionary trusts and CGT event E4 must be capable of happening to all the interests in the trusts. Practically speaking, this means both trusts are likely to be “fixed trusts” (in a non-tax sense); and

(d) the market values of the interests in the trusts after the rollover must be substantially the same as the market value of the interests in the trusts before the rollover.

There are also exceptions to these rules, including where the Recipient is a foreign trust, either trust is a public trading trust or both trusts have not made the same choices (called “mirror choices”) for tax purposes. One obvious point on the choice requirement is whether relief is unavailable in circumstances where the specified individual of the Transferor, for family trust election purposes, has deceased.

The operation of the rollover means that sub-division 126-G of the ITAA 1997 might be a suitable replacement to clone a “fixed trust” with “discretionary trust” unitholder/s. However, advisors should take account of the ATO’s earlier interpretation of the same beneficiary test from taxation ruling TR 2006/4. Structures that, at first blush, may appear to be the same were arguably not the same at all.

For instance, under the ATO’s earlier interpretation, a receiving trust did not have the same beneficiaries as a transferring trust if the transferring trust was a potential beneficiary of the receiving trust. In other words, the transferring trust could not be a beneficiary of itself and accordingly, relief was unavailable. There is also no clear authority about how sub-division 126-G of the ITAA 1997 may interact with the ATO’s more recent expressions of the tax law under TR 2018/6 and TD 2019/4, which relate to trust vesting and trust splitting.

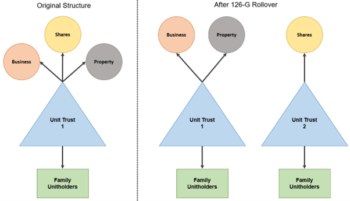

The following simplified example is illustrative of what could be possible.

Mrs and Mr Jones have two children, Sarah and John. Their relationship hasn’t always been harmonious. Sarah works in the family business. John doesn’t. The Jones’ want to provide for their children and grand-children, but recognise it won’t be easy because the assets (successful business, listed shares and growing property portfolio) are owned by one unit trust. The unit trust has family unitholders. The Jones’ want certain assets to be administered separately for succession planning purposes, including to manage family dynamics. The unit trust transfers the listed shares to a “cloned structure” enabling the Jones’ to separately administer the asset pools.

There are obviously various permutations to these types of circumstances which could mean relief is or is not available. One thing is clear. This is a rollover that should not be forgotten.

HWL Ebsworth Lawyers’ national tax group assists clients to manage all aspects of their tax compliance in respect of trusts. Please contact a member of our group to find out more.

This article was written by Vincent Licciardi, Partner and Tristan Shugg, Law Graduate.

Subscribe for publications + events

HWLE regularly publishes articles and newsletters to keep our clients up to date on the latest legal developments and what this means for your business. To receive these updates via email, please complete the subscription form and indicate which areas of law you would like to receive information on.

* indicates required fields